Why ULIPs (Unit Linked Insurance Plan) Fail

How does a ULIP work?

ULIPs are a category of life insurance plans that provide you with the benefit of growth of your

money along with a life cover. They do this by investing a part of your premium towards a life cover

for you, and the rest in funds of your choice. Most ULIPs give you the option to choose from

multiple equity and debt funds.

You can also invest in a mix of both types of funds as per your risk

appetite.

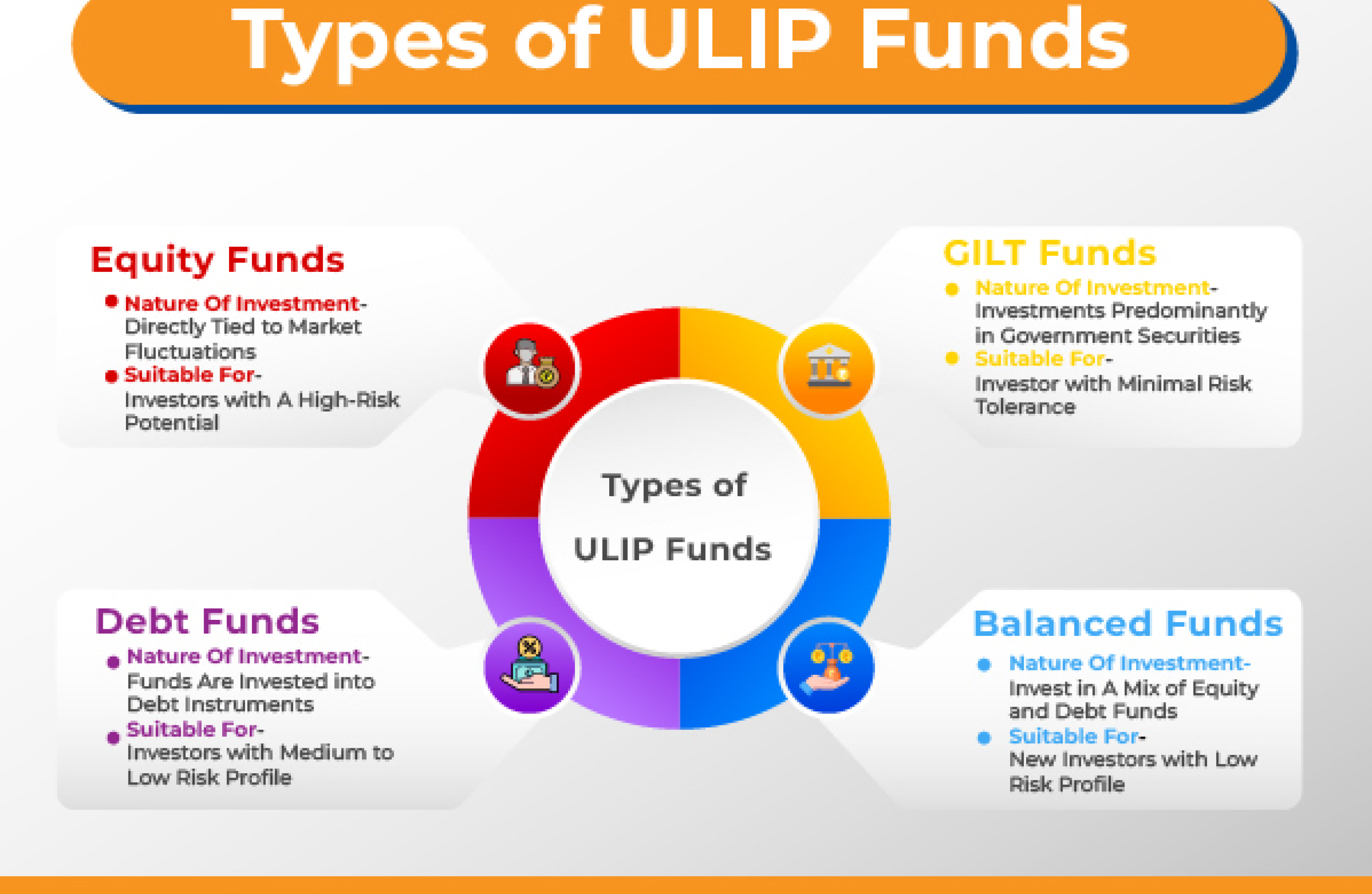

Types of Funds in ULIPs

-

Equity Funds

-

Debt Funds

-

Balanced Fund

-

Liquidity Funds

Equity funds are high-risk investments and include investments such as buying shares of companies. The change in the stock market directly influences the prices of the share, and hence, equity funds are suitable for investors willing to take higher risks.

These funds, also referred to as bond and income funds, carry a moderate level of risk and primarily invest in fixed-income and debt instruments such as corporate bonds, government bonds, and securities.

This is the most stable and preferred type of ULIP, blending equity instruments like company stocks with fixed-income instruments like bonds, resulting in a medium to high-risk profile.

Liquidity funds are low-risk in nature as they prioritise short-term market components such as bank deposits, commercial papers, and treasury bills. These funds are suitable for individuals who are unwilling to take risks with their money in equities or bonds.

FAQs about ULIP work

- If you stop paying premiums during the lock-in period, the policy may lapse or move to a "discontinued fund."

- After the lock-in period, the insurance cover may cease, but the investment portion remains active.

Comments